| What is a let-to-buy mortgage? | A let-to-buy mortgage allows you to rent out your current home and use the equity released to buy a new property. It is ideal for homeowners who want to move without selling their existing property. |

| How does a let-to-buy mortgage work? | You convert your existing residential mortgage into a buy-to-let loan while applying for a new residential mortgage on your next property. The rental income from your old home is considered when lenders assess affordability. |

| Who can apply for a let-to-buy mortgage? | Let-to-buy mortgages are available to homeowners who have sufficient equity in their current property, a good credit history, and meet affordability checks for both the rental and new residential mortgage. |

| Do I need a larger deposit for let-to-buy? | Yes, lenders usually require a minimum of 25% equity in your current home for the buy-to-let portion. For your new property, you may need at least 10% deposit depending on your credit profile and lender criteria. |

| Can first-time buyers get a let-to-buy mortgage? | No. Let-to-buy is specifically for existing homeowners. First-time buyers typically need a standard residential mortgage as they do not own a property to let. |

| What are the benefits of let-to-buy mortgages? | You can move quickly without waiting to sell, keep your current home as an investment, and potentially earn rental income while purchasing a new property. It also helps if the market conditions are not ideal for selling. |

| Are there risks with let-to-buy mortgages? | Yes. You will be responsible for two mortgages, and if your rental property remains empty or rental income drops, you must still meet both payments. Changes in interest rates can also affect affordability. |

| Do I pay higher interest rates for let-to-buy? | Typically, yes. The buy-to-let element of a let-to-buy mortgage often has slightly higher rates than standard residential loans due to perceived lending risk. However, rates are competitive and vary by lender. |

| Can I remortgage my property for a let-to-buy? | Yes. You can remortgage your current home onto a buy-to-let product while applying for a new residential mortgage. This process is common when moving home and retaining your property as an investment. |

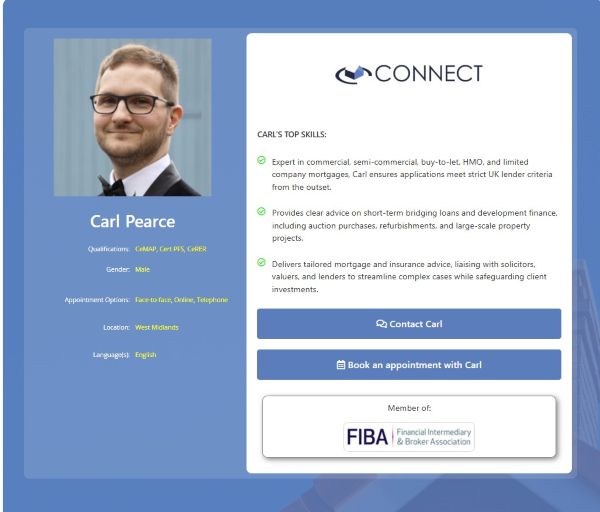

| Do I need a mortgage broker for let-to-buy? | It is strongly recommended. A qualified let-to-buy mortgage broker can compare both the residential and buy-to-let aspects, coordinate timing between lenders, and ensure you meet regulatory requirements. |

| Can I let my property before I complete my new purchase? | It depends on your lender’s policy. Most lenders require the buy-to-let mortgage to be in place before you let the property. A broker can help plan this sequence correctly. |

| Where can I find a let-to-buy mortgage broker near me? | You can use Connect Experts’ UK-wide broker finder to locate an FCA-authorised mortgage broker experienced in let-to-buy. Filter by location, language, and expertise to find the right adviser for your situation. |