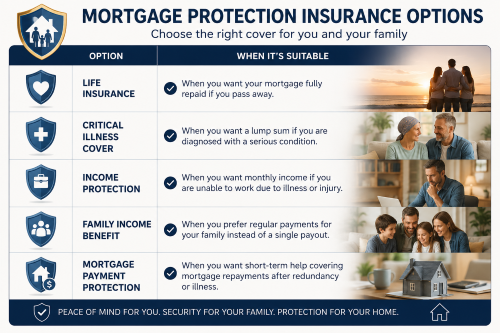

There are several protection insurance options available, including life insurance, critical illness cover, income protection, family income benefit and mortgage payment protection. Each policy works differently, so getting advice from a protection mortgage broker can help you compare suitable cover based on your mortgage balance, income, family situation, and monthly budget.

Life Insurance

Life insurance can help repay your outstanding mortgage if you pass away during the policy term. This type of mortgage protection cover is often considered by homeowners, first-time buyers and families who want to help ensure loved ones can remain in the home without the pressure of an unpaid mortgage.

Critical Illness Cover

Critical illness cover may provide a lump sum if you are diagnosed with a serious medical condition listed in the policy. This payment could be used to reduce or repay your mortgage, cover household bills, fund treatment-related costs, or provide financial breathing space while you recover.

Income Protection

Income protection insurance can provide a regular monthly payment if you are unable to work due to illness or injury. This can be especially useful if you rely on your income to cover mortgage repayments, rent, household bills and everyday living costs. It may also be valuable for self-employed workers, contractors and people without generous employer sick pay.

Family Income Benefit

Family income benefit is designed to provide regular payments to your family if you pass away during the policy term. Instead of a lump sum, this type of protection can provide ongoing financial support, helping your loved ones manage household expenses, childcare costs, and mortgage commitments.

Mortgage Payment Protection

Mortgage payment protection insurance can offer short-term support with mortgage repayments if your income is affected by illness, accident or redundancy, depending on the policy terms. This cover may help reduce the risk of falling behind on mortgage payments while you recover or look for new employment.

Getting the Right Protection Advice

The right protection policy depends on your personal circumstances, mortgage amount, employment status, dependants and existing cover. A protection insurance broker can explain your options, compare policies from different insurers and help you understand costs, exclusions, waiting periods and claim conditions.

Mortgage protection advice can help you clarify your cover options. Whether you need life insurance, critical illness cover, income protection, family income benefit or mortgage payment protection, the aim is the same: to help protect your home, support your family and provide financial peace of